Driving Automation Moves Mainstream as Level 2+ Systems Head for 77% of New Cars by 2031

Berg Insight forecasts a sharp rise in automated driving penetration, with Level 2 systems expected in 57.3 percent of new cars sold globally by 2031 and L2+ reaching a 31.0 percent attach rate.

The automated driving market is increasingly being shaped less by the race to full autonomy and more by the scaling of driver-assistance features that can be deployed across mainstream vehicle platforms. For automakers, the practical question is no longer whether ADAS (Advanced Driving Assistance Systems) will become common, but which automation level can be industrialised at volume, across regions, and within current regulatory and product-liability constraints.

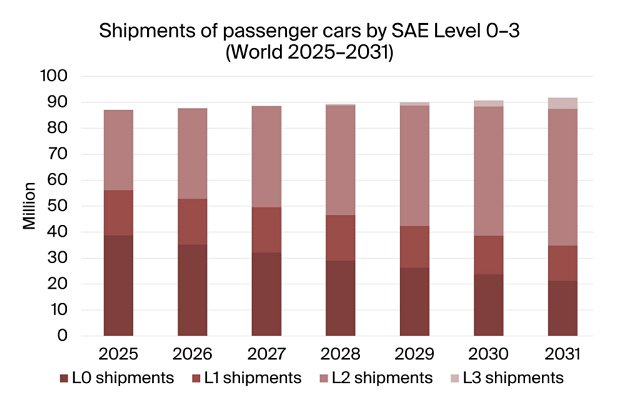

That is the context behind a new forecast from Berg Insight, which estimates that 55.6 percent of cars sold globally in 2025 met the requirements for SAE Level 1 automated driving or higher. By 2031, the analyst firm expects that share to rise to 76.9 percent. The more commercially significant shift, however, is in Level 2 functionality*: Berg Insight projects L2-capable new car sales to increase from 35.6 percent in 2025 to 57.3 percent in 2031.

L2+ becomes the strategic middle ground

The most distinctive element in the forecast is the expected acceleration of L2+, a subset of Level 2 systems that adds more advanced assisted-driving functions while remaining below conditional automation. Berg Insight estimates that 8.0 million new passenger cars sold in 2025 were equipped with L2+ ADAS, equal to a 9.2 percent attach rate. By 2031, that figure is expected to reach 28.4 million vehicles, or 31.0 percent of new passenger car sales.

This is not simply another forecast showing more ADAS in vehicles. Its importance lies in the relative balance between automation levels. Berg Insight expects only 4.8 percent of new cars sold in 2031 to feature Level 3 capabilities, while Level 4 passenger cars are not expected to scale in meaningful volumes before that year. In other words, the near-term automated driving market is being pulled toward driver-supervised systems rather than higher autonomy.

The logic is clear. L2 and L2+ systems can be fitted to a wider range of vehicles without requiring the same operational and regulatory framework as L3, where the vehicle can assume the driving task under defined conditions. This creates a different deployment profile for OEMs: the emphasis shifts from proving autonomy in limited domains to integrating sensors, compute, software and user experience into systems that can be sold at scale while keeping the driver engaged.

Berg Insight notes that BMW and Mercedes-Benz have both offered L3 systems, but have recently reduced their near-term emphasis on L3 and shifted focus toward more scalable L2+ systems. That repositioning is significant because it indicates that even premium brands with L3 experience are prioritising the automation level that can be expanded more broadly across product portfolios.

China’s ADAS push changes the competitive baseline

The report also underlines the role of Chinese OEMs in deploying sophisticated L2 and L2+ ADAS. Berg Insight identifies BYD Auto, Changan, Chery, Geely, GWM, Leapmotor, Li Auto, NIO, SAIC and XPeng among the leading Chinese players. Outside China, the report points to systems such as Tesla Full Self-Driving (Supervised), Ford BlueCruise, General Motors Super Cruise, Nissan ProPILOT 2.0/2.1, Toyota Teammate Advanced Drive, Hyundai Motor Group Highway Driving Assist 2, Volkswagen IQ.DRIVE/Travel Assist and Audi Adaptive Driving Assistant Plus.

For the IoT and connected-vehicle ecosystem, this matters because advanced ADAS is not a single-component market. Berg Insight describes a supplier landscape spanning Tier 1s, semiconductor providers, AD software companies, LiDAR specialists and mapping providers. Companies named in the report include Aptiv, Bosch, Denso, Magna International, Valeo and ZF Group on the Tier 1 side; AMD, Ambarella, Black Sesame Technologies, Horizon Robotics, Infineon, Mobileye, NVIDIA, NXP Semiconductors, Qualcomm, Renesas Electronics, STMicroelectronics and Texas Instruments in semiconductors; and Deeproute.ai, Huawei, Momenta, QCraft, Wayve, WeRide and Zhuoyu Technology in automated driving software and integrated solutions.

The practical implication is that ADAS growth will increase integration pressure across the vehicle technology stack. OEMs need to align compute platforms, perception software, sensor choices and map or localisation inputs. System integrators and Tier 1s will be asked to package this complexity into deployable vehicle programs. Semiconductor suppliers, meanwhile, are positioned not only as component vendors but as enablers of central compute architectures and associated electronic content.

LiDAR and mapping remain part of the higher-end ADAS discussion, with Berg Insight naming Hesai Technology, Innoviz, RoboSense and Seyond among LiDAR suppliers, and Amap, Dynamic Map Platform, HERE Technologies, NavInfo, Mapbox and TomTom among mapping and navigation platform providers. Their role will depend on how OEMs choose to differentiate L2+ offerings and how much capability they want to support beyond camera- and radar-based assistance.

The forecast therefore points to a market where commercial scale is likely to come from assisted driving rather than autonomy. For enterprises, fleet operators and industrial players evaluating future vehicle platforms, the key takeaway is to look closely at the automation level being offered, not just the branding. By 2031, the mainstream automated vehicle will still largely be a supervised driving system—but one with a much more complex technology supply chain behind it.

The post Driving Automation Moves Mainstream as Level 2+ Systems Head for 77% of New Cars by 2031 appeared first on IoT Business News.