Europe’s Smart Meter Market Shifts From Rollout Race to Technology Transition

Berg Insight estimates that two thirds of electricity customers in the EU27+3 had a smart meter by the end of 2025, with further growth expected through 2031. The next phase of the market will be shaped not only by new deployments, but by replacements and communications technology choices.

Smart metering in Europe is no longer a single deployment story. In some countries, utilities are still working through first large-scale electricity meter rollouts. In others, the discussion has already moved to second-generation devices, upgraded communications networks and the operational lessons learned from earlier programmes.

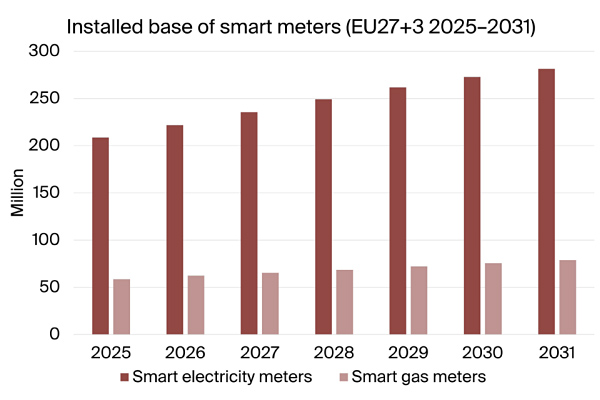

That split is the most useful lens through which to read Berg Insight’s latest assessment of the European smart metering market. According to the research firm, the EU27+3 region had around 209 million smart electricity meters installed at the end of 2025, equivalent to approximately two thirds of electricity customers. Berg Insight expects the installed base to grow at a compound annual growth rate of 5.1 percent and reach 85 percent penetration by 2031.

The forecast implies continued volume for meter manufacturers, communications module suppliers and systems integrators, but not a uniform opportunity across Europe. Berg Insight expects more than 131 million smart electricity meters to be deployed in the region during 2025–2031. A significant part of that demand will come from first-generation projects in countries including Germany, the UK, Poland and Greece, while replacement and second-generation activity is set to support shipments in markets such as Spain, France and the Netherlands.

A market split between first deployments and refresh cycles

What makes this forecast distinct from a typical smart metering market update is the clear separation between two different phases of European deployment. Berg Insight says first-generation smart electricity meters are expected to account for 65 percent of cumulative shipment volumes during the forecast period. By 2031, Central and Eastern Europe and Southeastern Europe are expected to account for 76 percent of Europe’s total first-generation shipments.

That matters because a first national rollout is not the same business as a second-generation replacement cycle. Initial deployments often involve large-scale field installation, customer coverage challenges and the establishment of meter data management processes. Second-generation projects, by contrast, tend to build on existing operational platforms and may place more emphasis on interoperability, continuity with installed infrastructure and migration risk.

The practical implication is that suppliers cannot treat Europe as a homogeneous smart metering market. OEMs selling meters into lower-penetration markets may face different cost, coverage and procurement priorities than vendors competing in mature Western European markets where utilities are upgrading established estates. System integrators, similarly, will need to support both greenfield-style deployments and migration projects where utilities are reluctant to disrupt existing back-office and communications architectures.

LPWA gains ground, but PLC remains part of the European architecture

The communications layer is another important part of the story. Berg Insight reports that standalone wireless connectivity options have gained traction and are expected to represent more than 50 percent of annual shipment volumes through most of the forecast period, peaking at about 62 percent in 2028. The firm identifies 3GPP-based LPWA technologies as the main driver of this growth, with shipments of LTE-M and NB-IoT electricity meters forecast to be in the range of 2.4 million to 6.1 million units during 2025–2031.

This does not mean that Europe is moving to a single wireless model. Powerline communications will remain significant, particularly in major countries preparing second-generation rollouts that are expected to build on existing communications platforms. Berg Insight notes that some of these markets may use upgraded or hybrid PLC-based approaches adapted to new requirements, with Italy cited as a comparable example.

The derived lesson for connectivity providers is that smart metering will continue to reward multi-technology strategies. Cellular LPWA offers a standards-based option that can reduce reliance on dedicated utility communications infrastructure in some deployments. PLC, however, retains value where utilities have already invested in it and where replacement programmes must preserve operational continuity. For industrial IoT vendors serving utilities, the opportunity is therefore not simply to replace PLC with cellular, but to help utilities manage mixed estates over long asset lifecycles.

Gas metering adds another layer to the European picture. Berg Insight expects the installed base of smart gas meters in the EU27+3 to increase from nearly 59 million units in 2025 to around 79 million by 2031, equivalent to 48 percent penetration. While smaller than the electricity meter base, this forecast reinforces the broader utility trend: connected metering infrastructure is becoming a long-term operational platform rather than a one-off compliance project.

For enterprises and industrial energy users, broader smart meter penetration should gradually improve the availability of granular consumption data, although the impact will depend on national market rules and utility data access models. For the IoT ecosystem, the more immediate takeaway is commercial and architectural: Europe’s smart metering market remains large, but its growth is becoming more segmented, more regional and more dependent on technology migration choices than the headline penetration figure alone suggests.

The post Europe’s Smart Meter Market Shifts From Rollout Race to Technology Transition appeared first on IoT Business News.